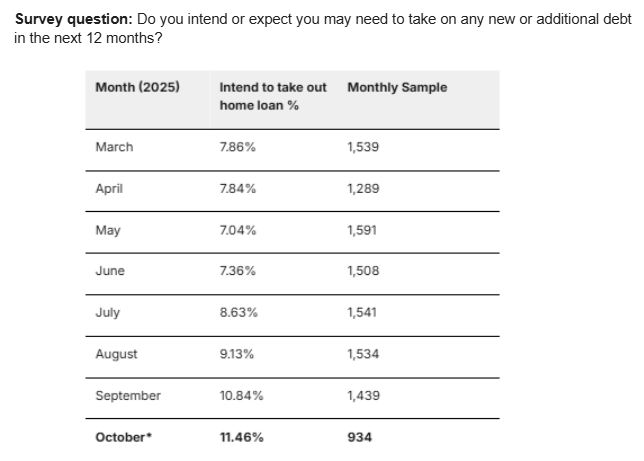

Home loan intentions among Australian consumers increased from 7.86% in March 2025 to 11.46% in October 2025, marking a 46% rise over eight months.

Data from 11,375 Australian consumers surveyed between March and October 2025 reveals a significant acceleration in home buying activity. Consumer intentions to take on home loans, plans to purchase property within 12 months, and financial priorities focused on saving deposits all increased substantially, suggesting a material shift in sentiment towards property ownership.

Key stats you need to know

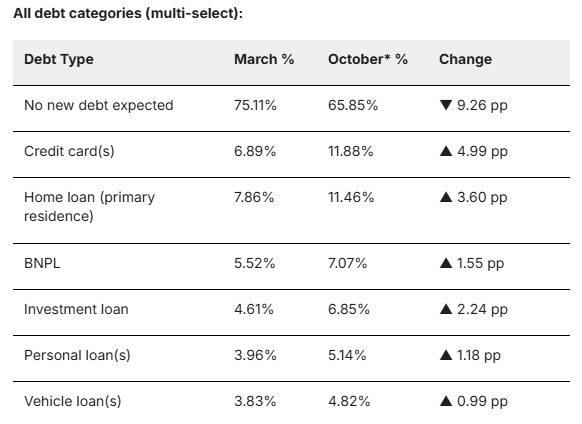

- The proportion of consumers expecting to take on home loans increased from 7.86% to 11.46% between March and October 2025, whilst those saying they expect no new debt declined from 75.11% to 65.85%.

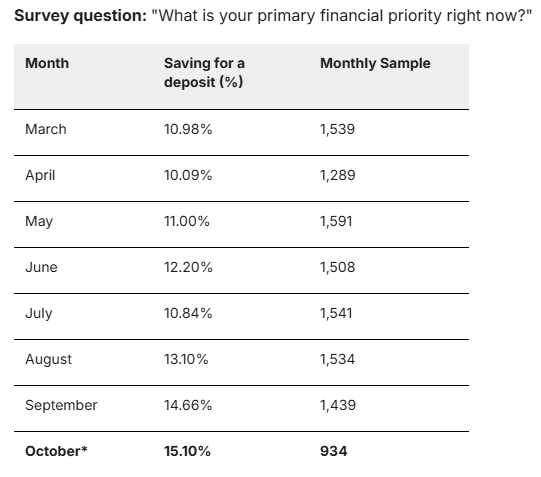

- Consumers prioritising saving for a house deposit as their primary financial goal rose from 10.98% to 15.10% over the eight-month period.

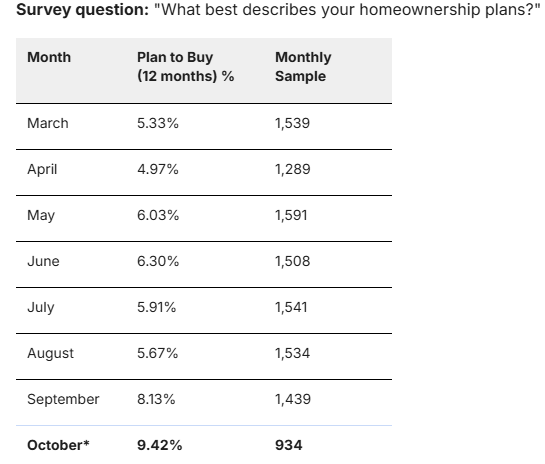

- Those planning to buy a home within the next 12 months surged from 5.33% in March to 8.13% in September, representing a 77% increase before policy changes took effect.

Home loan intentions peak in October at 11.46% of consumers, up from 7.86% in March

- In March 2025, 7.86% of Australian consumers expected to take on home loans for their primary residence within the next 12 months. By September 2025, this figure had increased to 10.84%, before reaching 11.46% in October 2025 (incomplete month).

- The proportion of consumers stating they do not expect to take on any new debt decreased from 75.11% in March to 68.59% in September. All debt categories surveyed showed increases over the period, with credit card intentions rising from 6.89% to 8.83% and investment loan intentions increasing from 4.61% to 5.70%.

- The acceleration in home loan intentions was particularly pronounced from July onwards, with the percentage nearly doubling from the low point in May (7.04%) to October (11.46%).

The normalising of debt expectations, particularly for property-related borrowing, signals a shift in consumer confidence about taking on financial commitments. The decline in those expecting no new debt represents approximately 1,000 additional consumers per 10,000 surveyed now anticipating debt obligations. This trend coincides with the spring property selling season and preceded the October 1, 2025 launch of the expanded First Home Guarantee scheme, which allows all first home buyers to purchase with just a 5 per cent deposit, with no income limits or caps on places, and higher property price thresholds.

"We're seeing consumers move from hesitation to action across multiple indicators simultaneously," says Michael Johnson, Director at Agile Market Intelligence. "When debt expectations, financial priorities, and purchase plans all trend in the same direction over eight months, that's not statistical noise. That's a genuine behavioural shift. The September acceleration is particularly interesting because it happened before the October 1 scheme launch, suggesting anticipation of policy changes was already influencing behaviour. First home buyers were positioning themselves ahead of the announcement."

Saving for a house deposit as a primary financial priority for 15% of Australians, up 5% since March

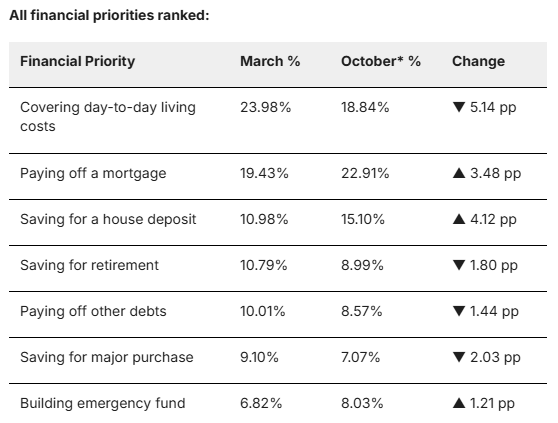

- The proportion of consumers identifying saving for a house deposit as their primary financial priority increased from 10.98% in March to 14.66% in September 2025. This represents the third-highest financial priority by September, behind covering day-to-day living costs (20.78%) and paying off existing mortgages (18.49%).

- Consumers prioritising day-to-day living costs declined from 23.98% in March to 20.78% in September, suggesting easing immediate financial pressure.

- The focus on mortgage repayment as a priority decreased slightly from 19.43% in March to 18.49% in September, whilst building emergency funds fell from 6.82% to 6.67%. Between June and September 2025, deposit saving showed consistent month-on-month growth, rising from 12.20% to 14.66%.

The reorientation of financial priorities towards property ownership occurred alongside reduced pressure from day-to-day expenses, creating a window for longer-term wealth-building goals. The sustained growth from June through September, rather than a single-month spike, indicates this shift reflects genuine changes in household financial planning rather than temporary sentiment. The expanded First Home Guarantee scheme, which removed income limits and place caps whilst raising property price thresholds, effectively lowered the deposit hurdle from 20 per cent to 5 per cent, potentially saving first home buyers tens of thousands of dollars in Lenders Mortgage Insurance and years of saving time.

"The convergence of declining cost-of-living pressure and rising deposit-saving priorities tells us consumers are finding breathing room in their budgets and directing it towards property," says Michael Johnson, Director at Agile Market Intelligence. "The expanded guarantee scheme fundamentally changed the economics of first-home buying. When you can now purchase with a 5 per cent deposit instead of 20 per cent, and avoid Lenders Mortgage Insurance entirely, you're cutting years off the deposit-saving timeline. The fact that nearly 15 per cent of consumers prioritised deposit saving even before the October launch suggests strong latent demand that policy has now unlocked."

Purchase plans accelerate after First Home Guarantee announcement

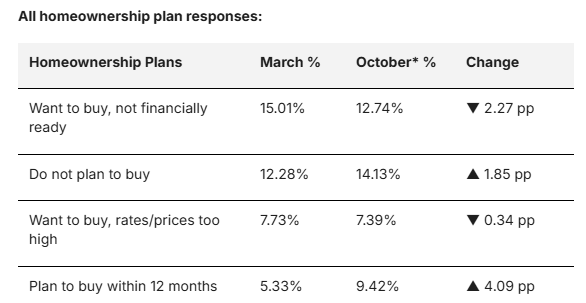

- Among non-homeowners, those planning to buy within 12 months increased from 5.33% in March to 8.13% in September 2025. This surge represents a 77% increase in immediate purchase intentions over the six-month period from March to September.

- The proportion of non-homeowners stating they want to buy but are not financially ready declined from 15.01% in March to 14.73% in September.

- Those citing high interest rates or property prices as barriers remained relatively stable, decreasing marginally from 7.73% to 8.20% over the same period.

- Purchase intentions remained relatively flat through May (5.67% to 6.30%), before accelerating notably in September (8.13%).

The acceleration in purchase plans during the second half of 2025 suggests external factors, including policy signals and seasonal market dynamics, influenced consumer decisions. The September surge preceded the October 1 launch of the expanded First Home Guarantee scheme, which was announced on August 25, 2025. This timing is significant: consumers began increasing their 12-month purchase intentions in the weeks immediately following the policy announcement, suggesting the removal of income limits, place caps, and the reduction of the deposit requirement from 20 per cent to 5 per cent created immediate shifts in consumer planning. The Government estimated first home buyers using the scheme would avoid approximately $1.5 billion in Lenders Mortgage Insurance costs in the first year alone.

"The timing of this acceleration matters," says Michael Johnson, Director at Agile Market Intelligence. "The September surge in concrete purchase plans came immediately after the August 25 guarantee scheme announcement but before the October 1 implementation. This shows how quickly policy changes can shift consumer behaviour when they materially improve affordability. A first home buyer in Brisbane could suddenly purchase a $1 million property with $50,000 instead of $200,000. That's not just incremental improvement, that's transformational for household budgets."

About the research

This analysis draws on data from Consumer Pulse, a longitudinal tracking study of Australian consumer financial attitudes and behaviours. The research surveyed 11,375 Australian consumers who completed responses between 11 March 2025 and 16 October 2025. Monthly sample sizes ranged from 934 to 1,591 respondents, with October 2025 representing an incomplete month (data through 16 October only). All percentages are calculated against total monthly respondents to enable direct comparison across time periods.

Consumer Pulse is an always-on tracker of over 1,500 Australian consumers every month developed by Agile Market Intelligence to monitor consumer sentiment, financial stress, and behavioural shifts across key household segments. The survey provides a real-time view of financial wellbeing in Australia, segmented by debt status and home ownership.