Consumer financial products span the full spectrum of banking needs from everyday transaction accounts and credit cards to home loans representing the largest financial commitments most Australians will make. Each product category tells a different competitive story.

Agile Market Intelligence’s Consumer Pulse survey asks around 1,500 Australian consumers every month about the financial products they hold and which institutions they bank or transact with. The latest results confirm Commonwealth Bank’s (CBA) commanding position across all consumer banking categories, but beyond CBA’s dominance, meaningful insights emerge about how other lenders compete. While some markets are tightly controlled by major banks, others show more diverse participation from regional and specialist lenders carving out substantial market share.

Key stats you need to know

- ANZ holds second position across all major lending categories in Q3 2025, maintaining consistent competitive strength behind Commonwealth Bank.

- ING demonstrates the strongest non-major presence in everyday banking (9% market share) and personal loans (5%), showing digital banks can compete effectively outside traditional lending.

- St. George emerges as the top performing non-major for credit cards and mortgages with 5% market share in either space, outpacing other regional lenders in core lending products.

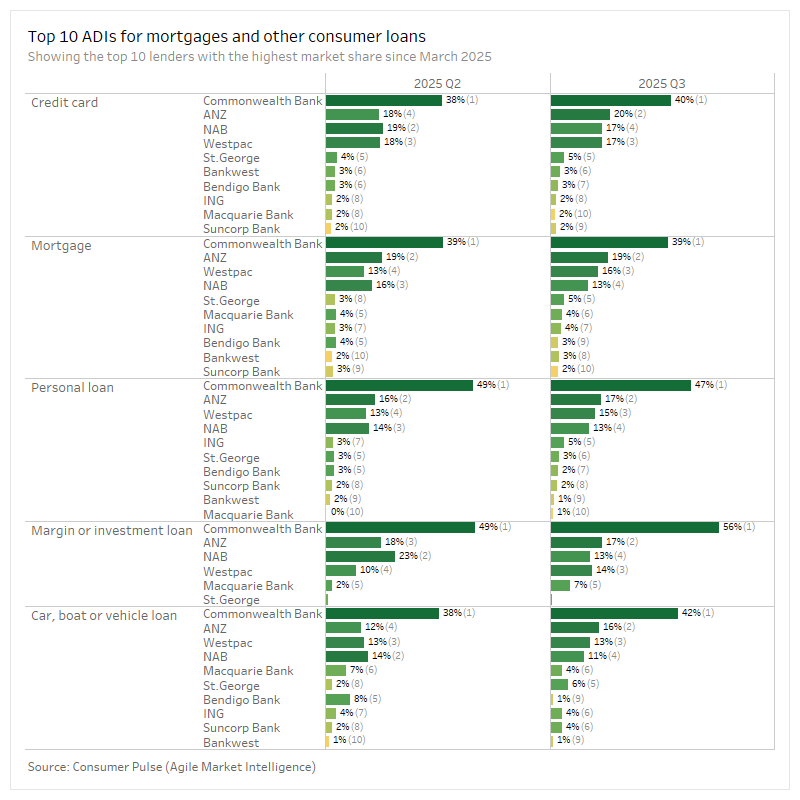

Credit cards remain a major bank stronghold

- ANZ (20%), Westpac (17%), and NAB (17%) secure the top positions behind Commonwealth Bank (40%), maintaining the big four’s traditional dominance.

- St. George (5%), Bankwest (3%) and Bendigo Bank (3%) represent the strongest non-major presence in the credit card market.

- ING, Suncorp Bank and Macquarie Bank, all with 2% market share, complete the top 10 most used credit card providers.

The credit card market shows the clearest major bank dominance with the big four occupying large slices of market share with ANZ inching its way to second place this quarter. Regional and digital banks maintain presence but at a considerably smaller scale, suggesting consumers still gravitate toward established players for credit products.

Mortgage market follows similar hierarchy with subtle competitive shifts

- ANZ maintains second place with 19% market share, while Westpac and NAB show more competitive parity quarter-on-quarter, with 16% and 13% for Q3, respectively.

- St. George (5%), Macquarie Bank (4%) and ING (4%) demonstrate stronger relative positioning in mortgages compared to their credit card market share.

- Bendigo Bank (3%), Suncorp Bank (32%) and Bankwest (23%) complete the top 10 home loan providers, also with stronger relative positioning.

Home lending follows a comparable hierarchy to credit cards, but with some notable competitive shifts worth noting. St. George, ING and Macquarie show more successful market penetration in mortgages, suggesting these lenders have built stronger value propositions in home lending than in consumer credit products. Whether through competitive rates, broker relationships, fast turnaround times or other competitive advantages, these lenders have captured meaningful market share in Australia’s largest consumer lending category.

“Major banks maintain dominance on consumer lending products. But for home loans, we see a healthy market share for non-majors like St. George, ING, and Macquarie, that translates into large loan books in the mortgage space.” said Michael Johnson, Director at Agile Market Intelligence.

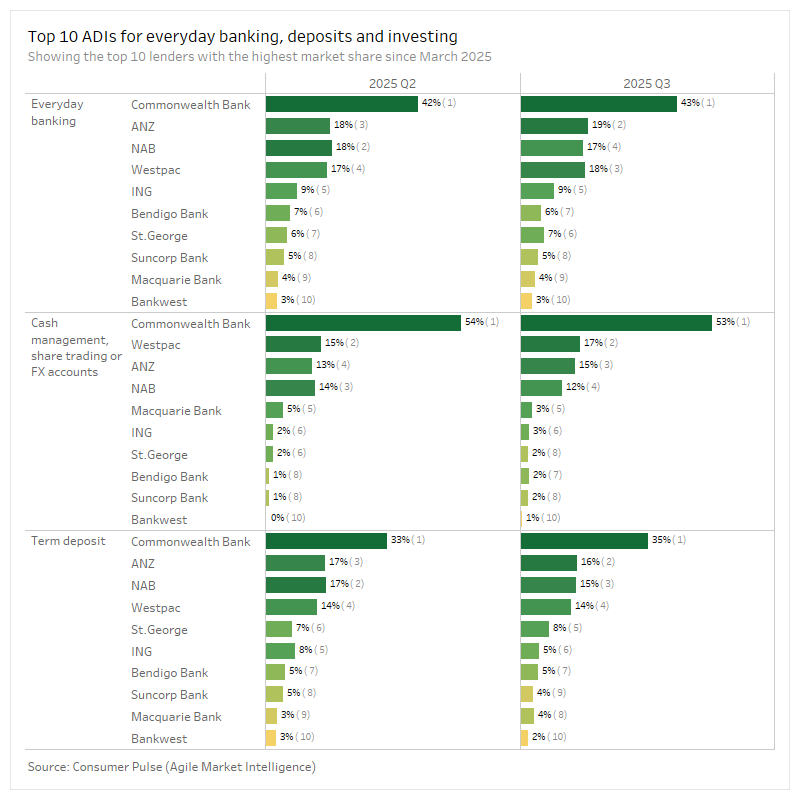

Everyday banking attracts strongest non-major participation

- ANZ (19%), Westpac (18%) and NAB (17%) are in tight competition for second to fourth positions in market share, while CBA (43%) stays in the lead.

- ING (9%), St. George (7%), Bendigo Bank (6%), Suncorp Bank (5%) carve out substantial portions of the market share, larger than their market penetration in consumer lending.

- Macquarie Bank (4%) and Bankwest (3%) complete the top 10 with impressive market shares in the everyday banking space.

Transaction accounts show consumers’ greatest willingness to bank with non-majors. Compared to the lending space, majors have similar relative market share next to CBA (43% in Q3), with each having about half (17-19%) the market share. However, non-majors show more competitive market shares next to the big four. ING’s particularly strong showing (9%) demonstrates digital banks have successfully competed for everyday banking relationships, even as they maintain smaller presences in lending categories.

Specialised products reveal niche positioning

- Cash management is dominated by CBA (53%), with Westpac (17%), ANZ (15%) and NAB (12%) following in the investment/management category. Macquarie tops non-majors with its 3% market share.

- Term deposits is another product with a more level playing field among majors and non-majors alike, with St. George (8%) and ING (5%) being the top performing non-majors.

The specialised product categories paint an interesting picture of competitive dynamics beyond traditional lending. Similar to everyday banking, the market for term deposits is another product with more ADI diversity and better market penetration compared to their performance in the lending space. It reinforces an emerging theme where Australian consumers demonstrate greater willingness to diversify their banking relationships when it comes to deposits and transaction accounts compared to their borrowing decisions.

"While the majors hold much of the lending space, deposits and transactions show a different competitive story. Non-majors have successfully built trust for deposits and everyday banking, as shown by their stronger presence in the market," said Michael Johnson.

About the research

This article is based on 7,965 responses from Agile Market Intelligence’s Consumer Pulse survey of consumers with at least 1 financial product, collected across March to November 2025 (to date). We tallied the number of responses by Authorised Deposit-Taking Institutions (ADIs), with each respondent possibly having multiple financial products with multiple providers. The Consumer Pulse is a monthly tracker of over 1,500 Australian consumers developed by Agile Market Intelligence to monitor consumer sentiment, financial stress, and behavioural shifts across key household segments. The survey provides a real-time view of financial wellbeing in Australia, segmented by debt status, home ownership, and other demographics.