Consumer Pulse is an always-on survey of Australian consumers that collects information on their attitudes, experiences and priorities towards their finances and financial institutions. The survey tracks consumer sentiment based on their financial security/anxiety, their perceived financial health relative to a year ago, and their reported household cash flow for the current month. Mortgage holders are currently enjoying a period of positive cash flows and a healthy financial situation, a breathing room afforded by the price drop that occurred in December 2025. Despite this, there is an increasingly growing trend of mortgage holders growing worried about their finances, which may be attributable to the recent cash rate increase earlier this February.

Key stats you need to know

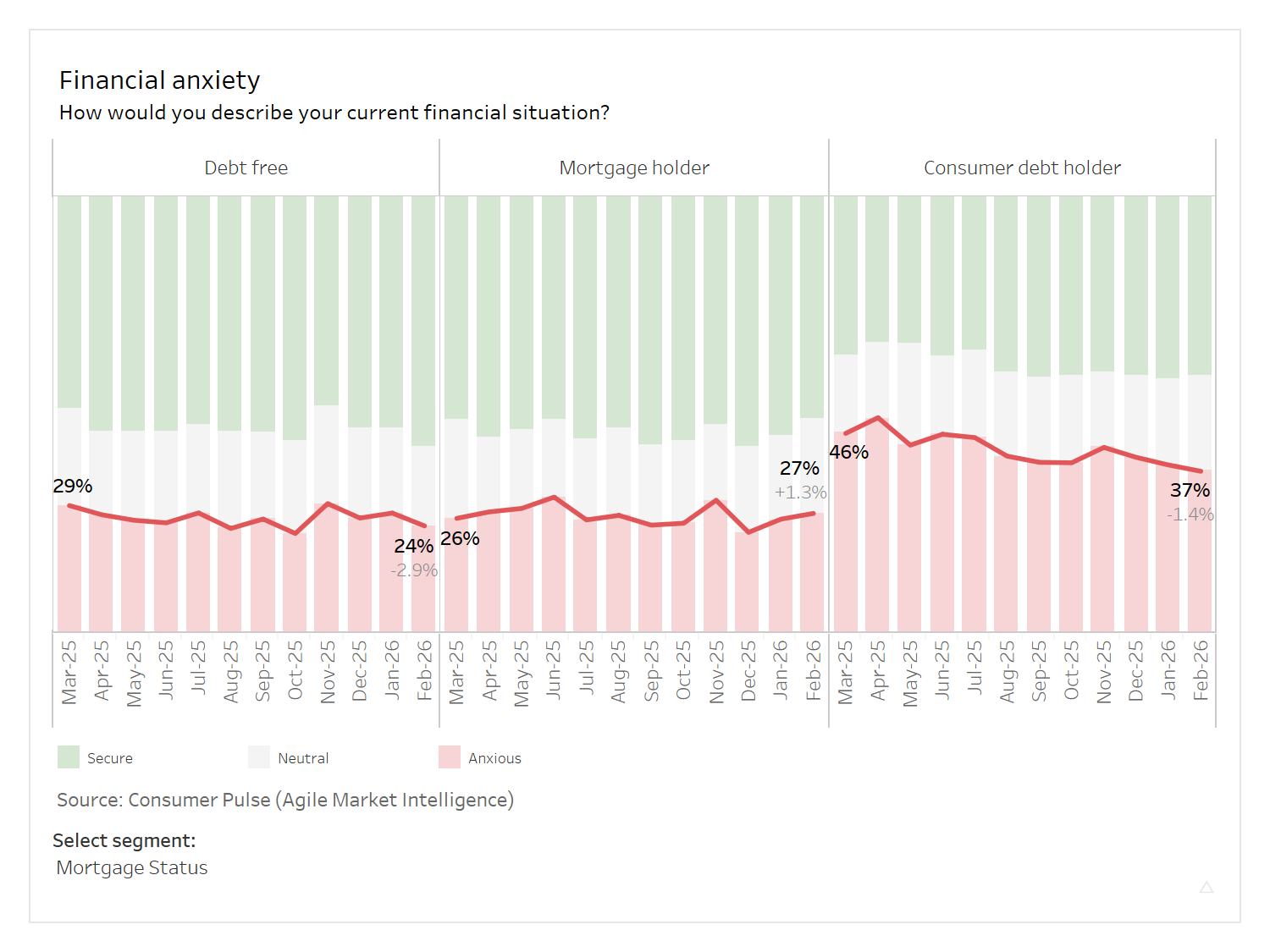

- 27% of mortgage holders are anxious about their current financial situation.

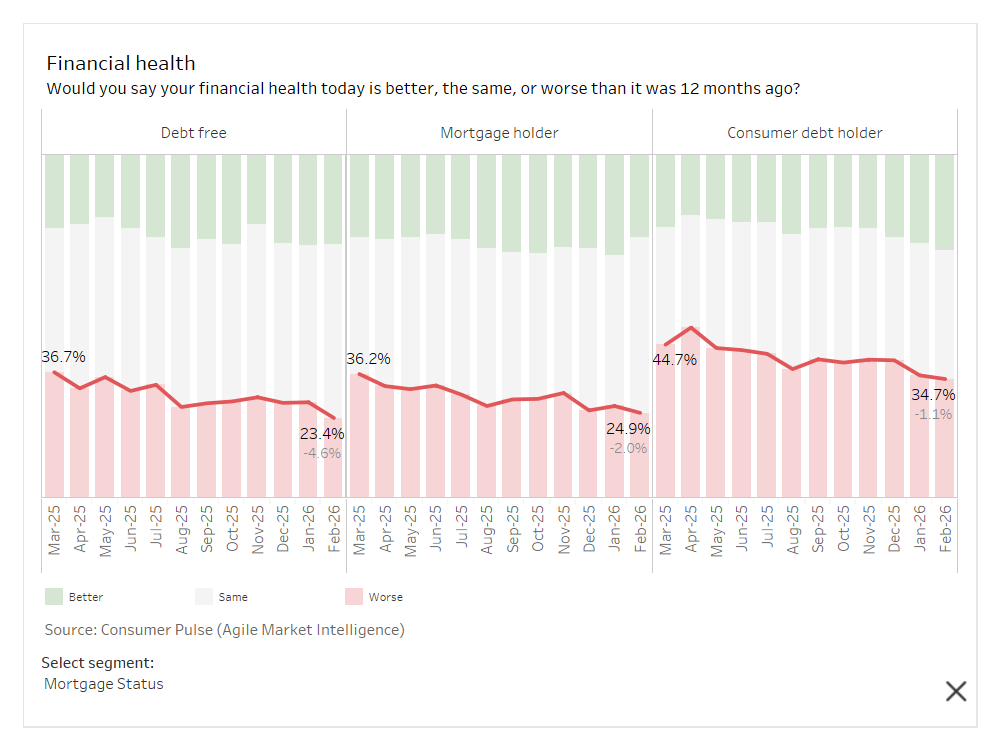

- The number of mortgage holders who believe their financial circumstances are worse compared to 12 months ago has increased by +0.2%.

- Debt-free holders reported the highest positive cash flow this month (+20.4).

Over 1 in 4 mortgage holders are worried about their financial situation

- Debt-free households felt the highest decrease in financial anxiety across the board, dropping by -2.9%.

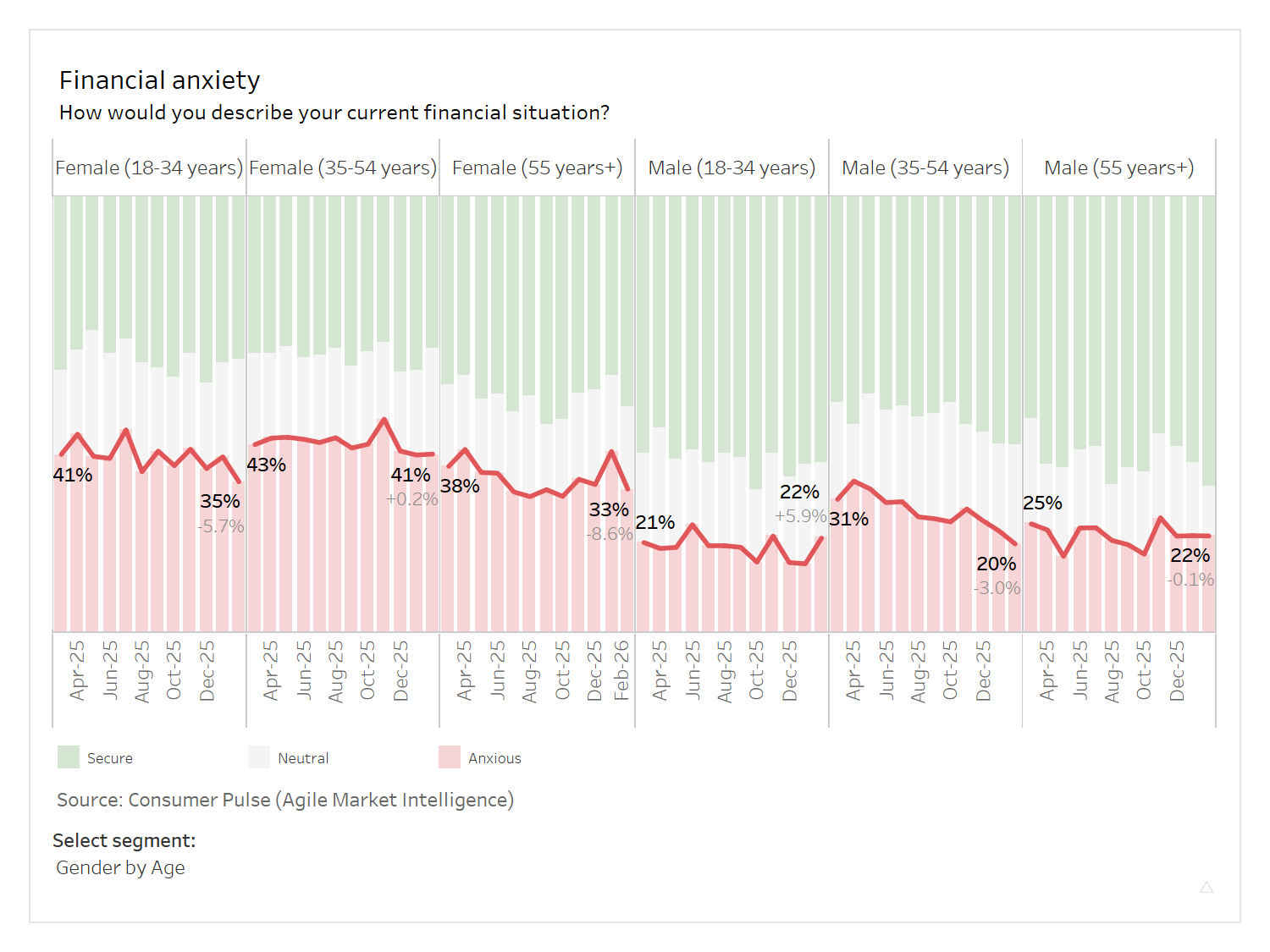

- Females aged 55 years old and above saw the steepest decrease in financial anxiety at -8.6%.

- Males aged 18-34 years old are growing increasingly worried about their finances, having risen by +5.9%.

Based on debt status, the segment feeling the most anxiety at the start of the year is consumer debt holders (37%), followed by mortgage holders (27%) and debt-free households (24%). Interestingly, consumer debt holders and debt-free households reported a decrease in financial anxiety in February 2026 by -1.4% and -2.9%, respectively. Whereas for mortgage holders, their financial anxiety increased by +1.3%. Mortgage holders feeling more worried could be attributable to the fact that several banks have increased their interest rates in lieu of the increased cash rate earlier this month.

Across the various age and gender segments, females are generally more anxious about their financial situation compared to males. However, most groups saw a decrease in their financial anxiety, spanning from a -0.1% to -8.6% reduction. The groups with increased anxiety are females aged 35-54 years old (+0.2%) and males aged 18-34 years old (+5.9%).

72% of mortgage holders view their finances has improved or remained the same compared to 12 months ago

- Around 2 in 3 consumer debt holders feel that their financial situation has either improved or remained the same.

- The number of debt-free Australians who feel their circumstances have worsened has decreased by -2.3%.

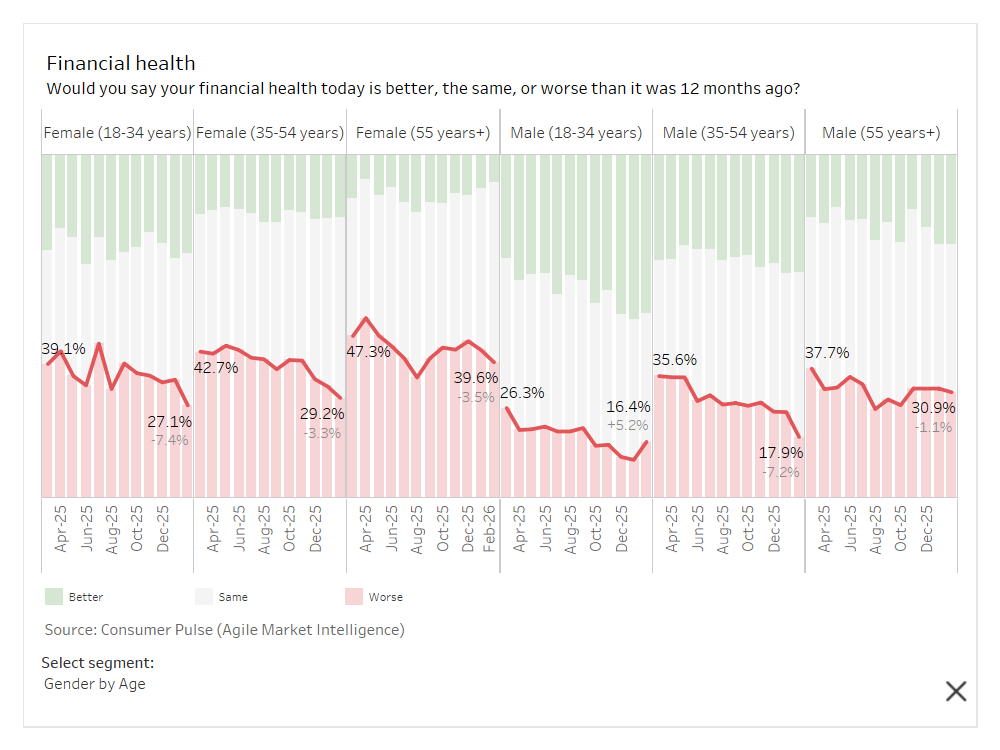

- Males 18-34 years old believe that their finances have changed for the worse, an increase of about 5.2% compared to January 2026.

Debt-free Australians saw the steepest improvement, seeing -2.3% are less worse off in their financial state compared to the previous month. The largest group of financially anxious Australians are consumer debt holders, with 35% of them expressing concern over their situation. In the middle lie the mortgage holders, where 27% believe their situation is worse off compared to a year ago.

Most of the age and gender segments state that their financial situation has remained or improved compared to twelve months ago, except for the youngest male cohort (+5.7%) and the eldest female segment (+1.7%). The data shows a downward trend in people feeling their finances have worsened, with the steepest decline being the youngest female cohort (-6.1%).

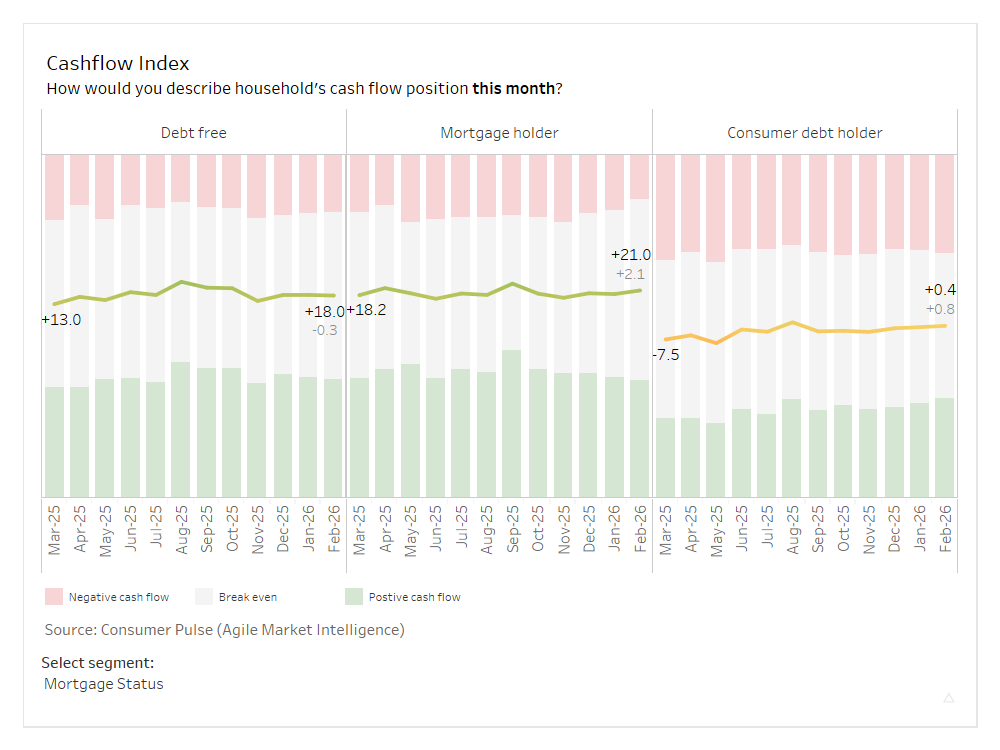

Debt holders have the highest increase in positive cash flow at +20.4

- Mortgage holders are the only segment to have reported a decrease in their cash flow (-1.6) in February.

- Females aged 55 years old and above have the lowest negative cash flow across the board at -7.8.

- Males 55 years old and above saw the steepest negative cash flow, seeing a decrease of -6.7.

Debt-free Australians boast the highest cash flow at +20.4, along with the highest increase of +2.0. Mortgage holders follow second with a cash flow of +17.3, but it is the only segment to have seen a decrease (-1.6). Consumer debt holders saw a recovery in February, with a cash flow of +0.3, having increased from the negatives by +0.7 compared to last January 2026.

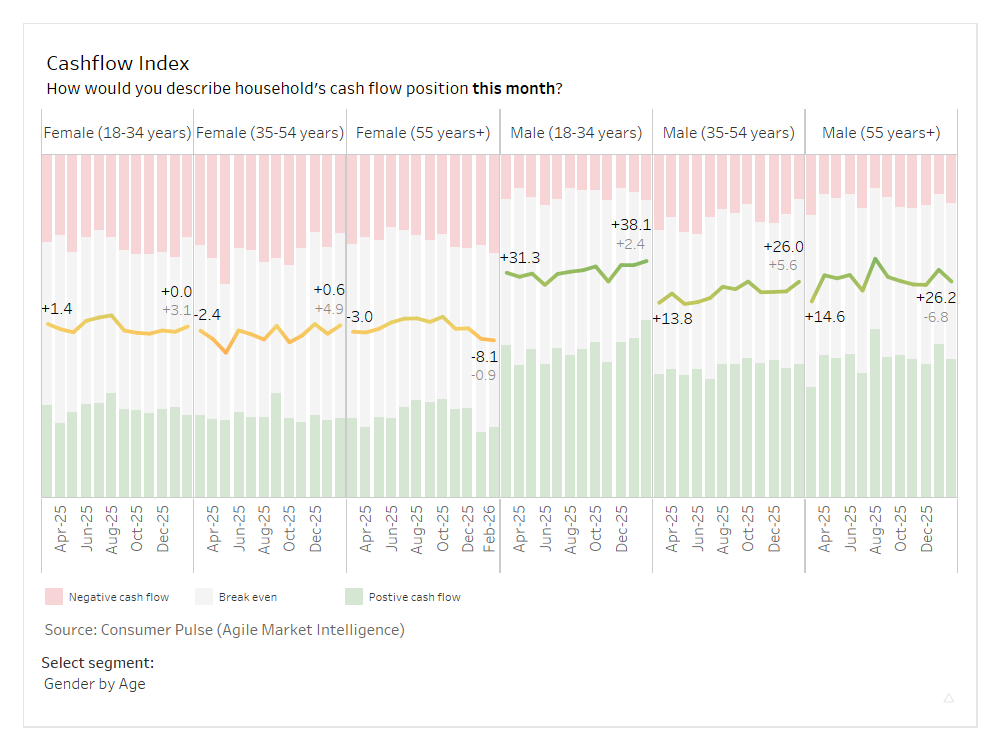

Males generally report higher positive cash flow compared to females. Alternatively, Males aged 18-34 years old boast the highest positive cash flow at +35.5. Among the females, those aged 35-54 years old peaked with a cash flow of +1.9, seeing a steep increase of +6.2. Alternatively, the segment with the steepest negative growth is males aged 55 years and above, having seen a decrease of -6.7.

About the research

This article is based on findings from Agile Market Intelligence’s Consumer Pulse survey, conducted from March 2025 to February 2026. The survey collected responses from 17,389 Australian consumers, weighted to reflect national population profiles by age, gender, and state. The survey gathers about 1,500 responses monthly. As of the time of writing, 752 responses were gathered for February 2026.

The Consumer Pulse is a monthly tracker developed by Agile Market Intelligence to monitor consumer sentiment, financial stress, and behavioural shifts across key household segments. The survey provides a real-time view of financial wellbeing in Australia, segmented by debt status, home ownership, and other demographics.