The RBA raised the cash rate to 4.10%, the second 25 basis point increase of the year. Ahead of the March 17 announcement, Australian households had already begun rapidly deprioritised savings in March, with 10% more mortgage holders shifting back to prioritising debt repayment. Across all segments, the proportion of consumers prioritising day-to-day expenses also rose, hinting at increasing cost-of-living pressures.

Agile Market Intelligence’s Consumer Pulse survey tracks the financial priorities of around 1,500 Australian consumers each month, capturing behavioural shifts across mortgage holders, consumer debt holders and debt-free households.

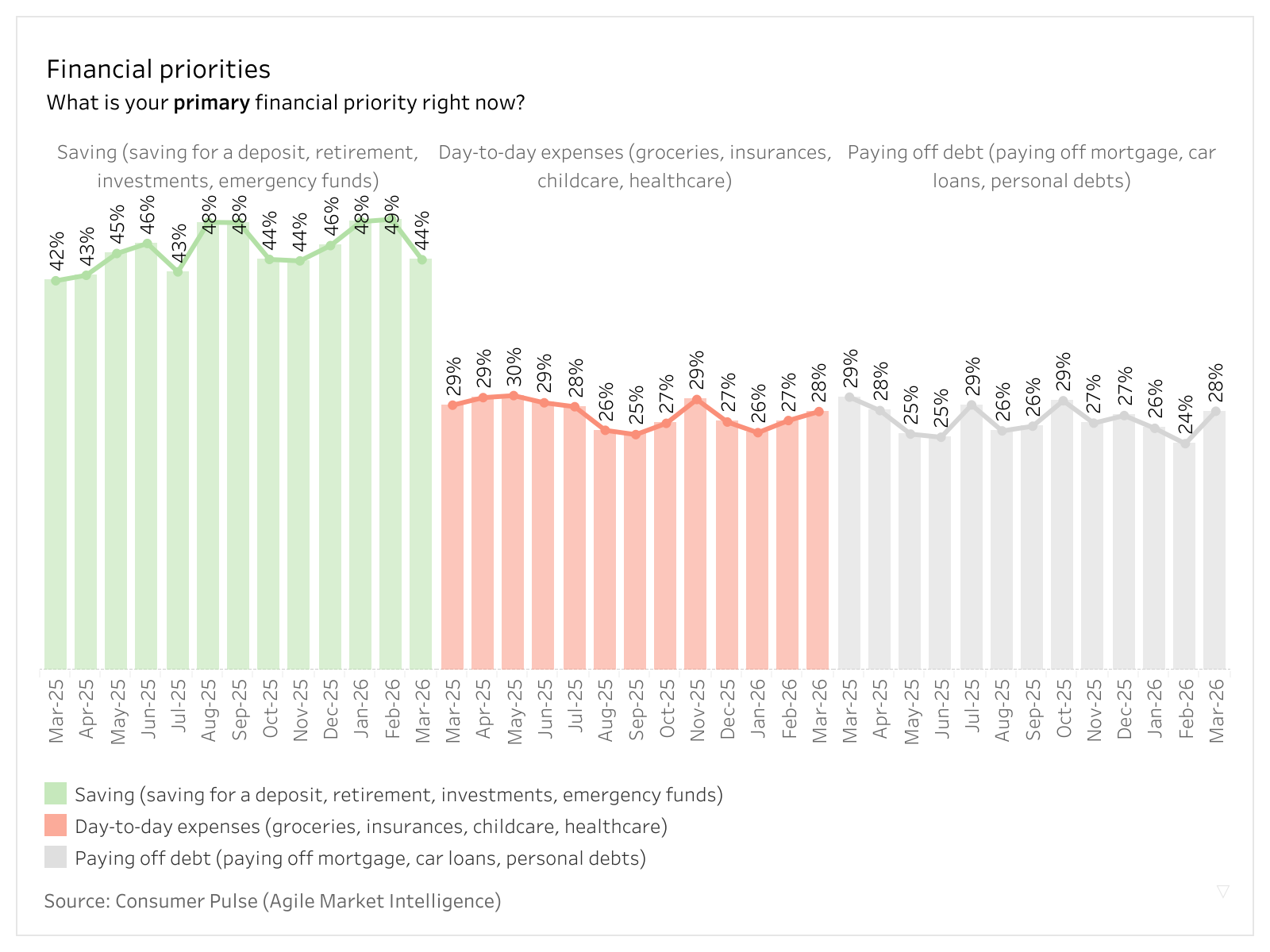

Key stats you need to know

- Australian households prioritising debt repayment grew 4% overall, and 10% among mortgage holders specifically.

- Mortgage holders prioritising day-to-day expenses decreased by 1% in March, despite a 2% increase among all households.

- Consumers prioritising savings has declined by 5%, a trend reflected across all debt statuses.

In a backdrop of rising interest rates and global economic uncertainty, the share of Australians with saving as their top financial priority fell to 44% of respondents, down 5% from the previous month. The remaining households are evenly split between prioritising day-to-day expenses and paying off debt at 28% each. Those prioritising debt repayment grew 4% from February, and the proportion prioritising daily expenses continued to rise.

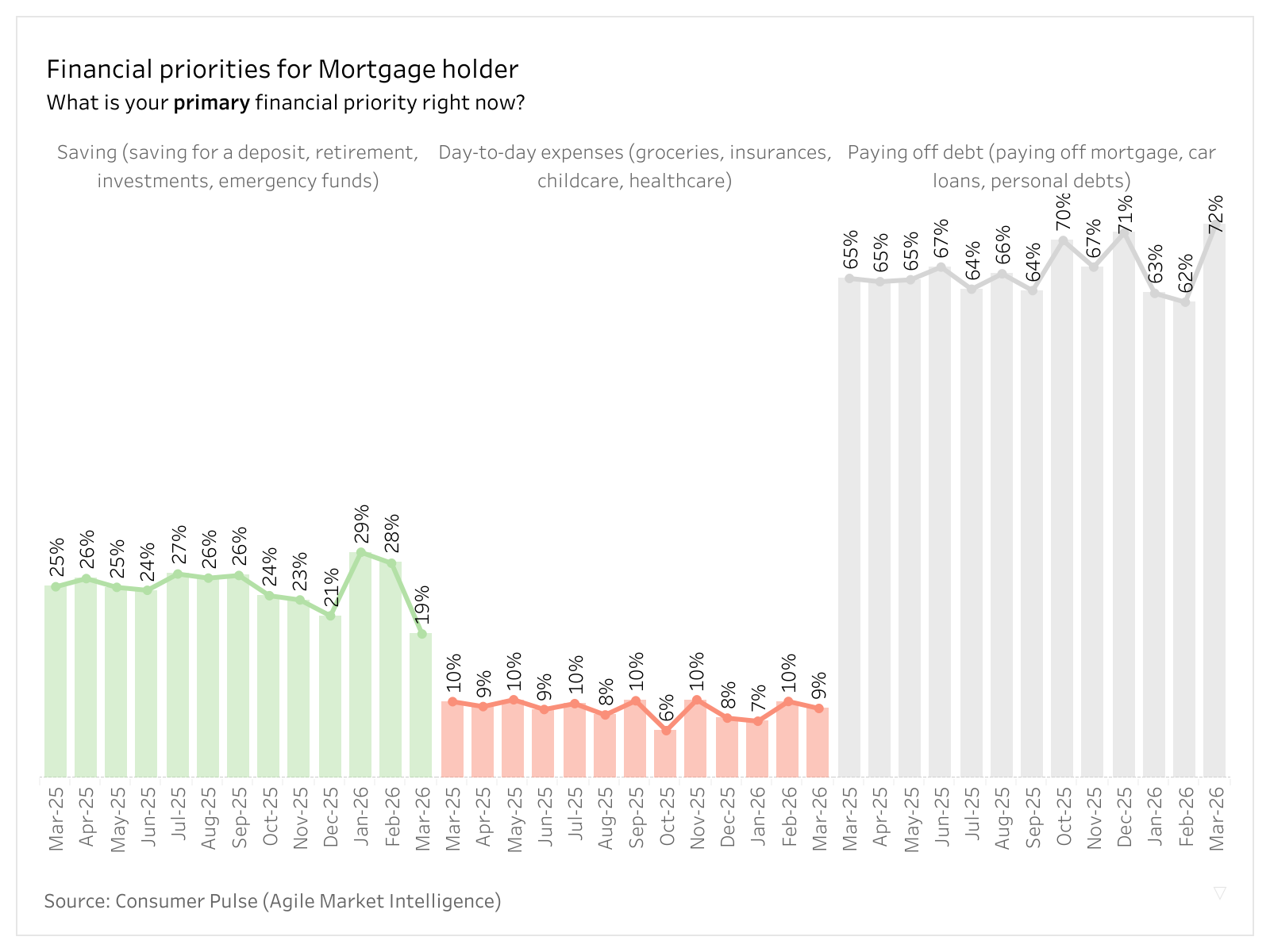

Mortgage holders record largest shift in financial priorities

- 72% of mortgage holders now cite debt repayment as their primary financial priority, up 10% from February. This is the highest single-month shift observed in the past year.

- Only 19% of mortgage holders are now prioritising savings, down 9% from the previous month.

- Mortgage holders prioritising day-to-day expenses edged down 1 percentage point.

The data points to deepening financial stress among mortgage holders, who doubled down on debt repayment in March. While the proportion of Australians prioritising day-to-day expenses continued to rise gradually, mortgage holders were the only group to record a decline in this measure, albeit small. This underscores that the direct pressure of rate hikes outweighs broader economic headwinds, including volatility in oil prices, for this segment. With only 19% prioritising saving (roughly 1 in 5), there is little room for financial planning beyond repayments for this group. It is also the lowest the ‘saving’ proportion has been over the past year.

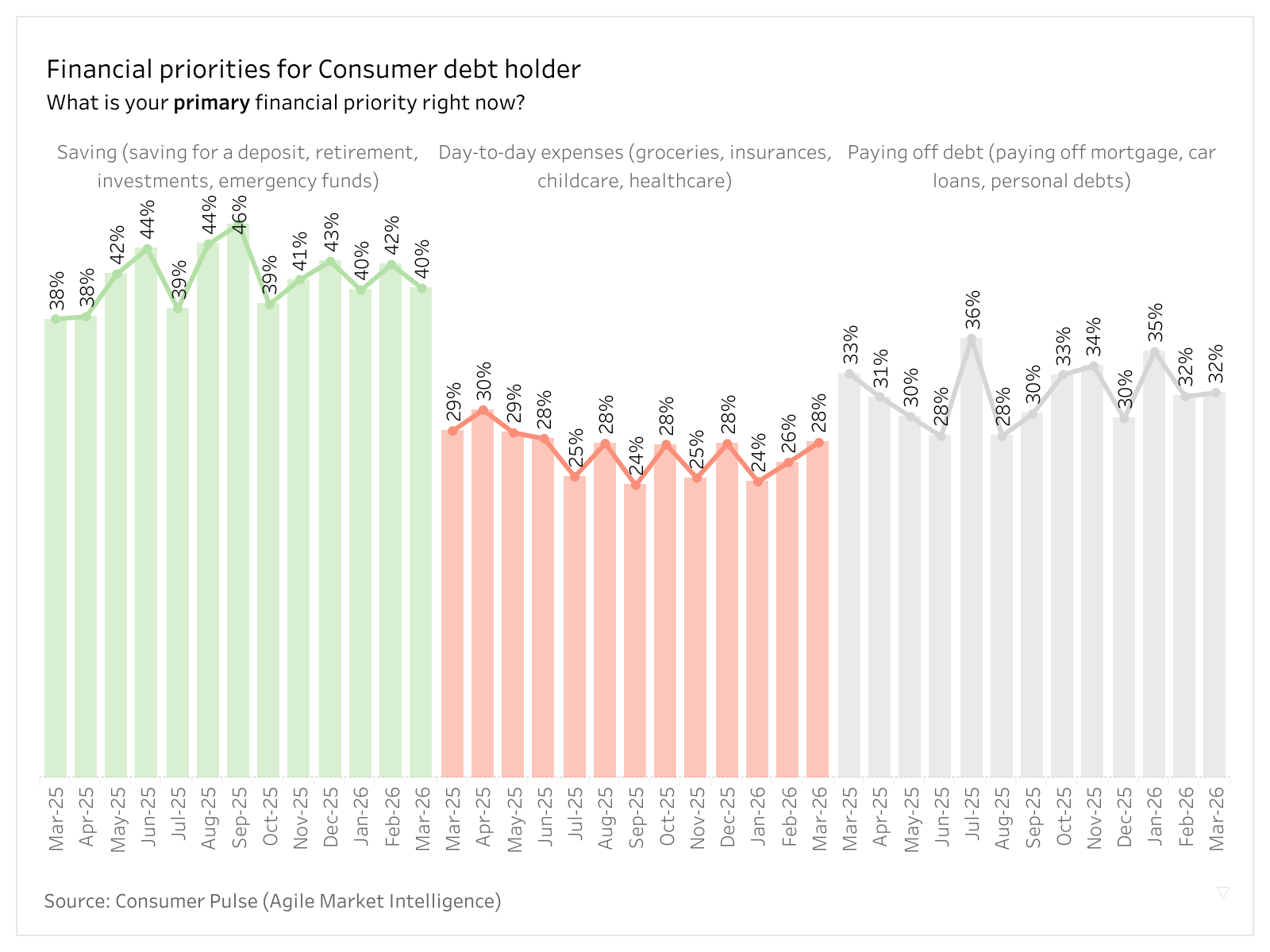

Day-to-day expenses increasingly prioritised by consumer debt holders

- 28% of consumer debt holders prioritised day to day expenses in March, up 4% since the start of the year. The shift comes from a decline in household prioritising savings.

- One-third of consumer debt holders are prioritising debt repayment in March, unchanged from February.

While the shift is less dramatic, consumer debt holders showed a steady increase in prioritising day-to-day expenses. Unlike mortgage holders who are consolidating around debt repayment, this segment appears to absorb the cost of living pressures more broadly, which could signal greater vulnerability to economic shifts down the line.

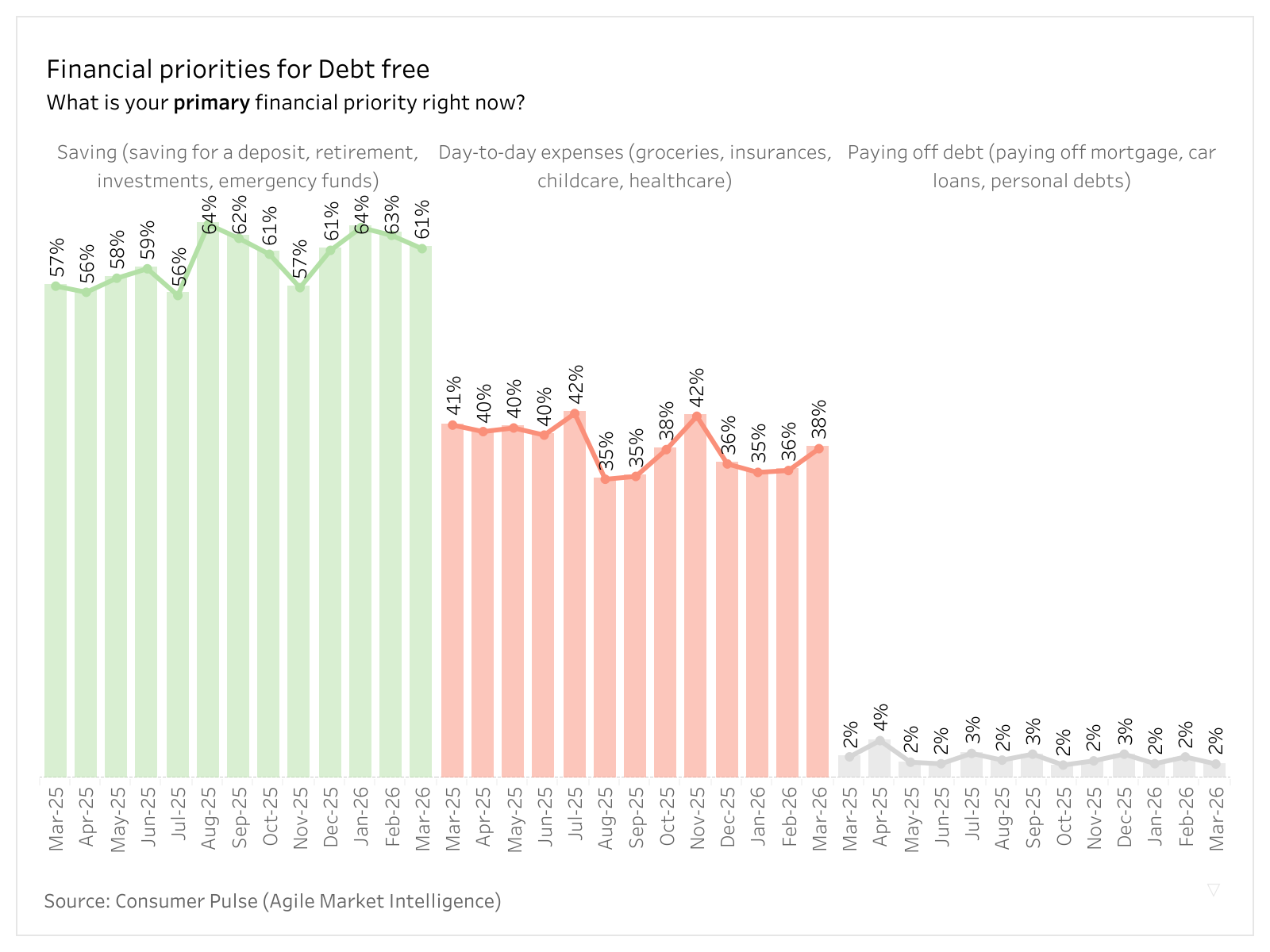

Debt-free households: a lagging indicator to watch

- The largest segment (61%) of debt-free households cited saving as their primary financial priority.

- The portion of consumer debt holders prioritising day-to-day expenses is at 38%, which has risen 4 percentage points since the start of the year.

Debt-free households (those without mortgages or consumer debt) remain in a position of relative financial stability, with 6 in 10 prioritising saving. However, this segment is not entirely insulated from cost-of-living pressures, as debt-free households prioritising day-to-day expenses has also grown 2%in March. As rate hikes and economic pressures compound, this segment could represent a lagging indicator of broader financial stress that is worth watching in the coming months.

"With only 1 in 5 mortgage holders prioritising saving, we're watching financial buffers erode in real time. If rate pressures persist, the ripple effects on broader consumer spending could be significant," said Michael Johnson, Director at Agile Market Intelligence.

About the research

Agile Market Intelligence tracks the financial priorities of Australian households through its Consumer Pulse survey. Conducted across March 2025 to March 2026 Australians holding a range of financial products including mortgages, loans, credit cards and investment accounts were asked about their top financial priority for the current month. Results were weighted to reflect national population profiles by age, gender, and state.

Consumer Pulse is a monthly tracker of over 1,500 Australian consumers developed by Agile Market Intelligence to monitor consumer sentiment, financial stress, and behavioural shifts across key household segments. The survey provides a real-time view of financial wellbeing in Australia, segmented by debt status, home ownership, and other demographics. Data for the current month comprises 742 responses collected from 1st to 16th of March.