The 2025 Agile Market Intelligence Legal Tech Review reveals that half of legal firms use practice management and legal operations platforms. However, satisfaction is falling behind, and negative sentiment may be undermining loyalty.

Key stats you need to know

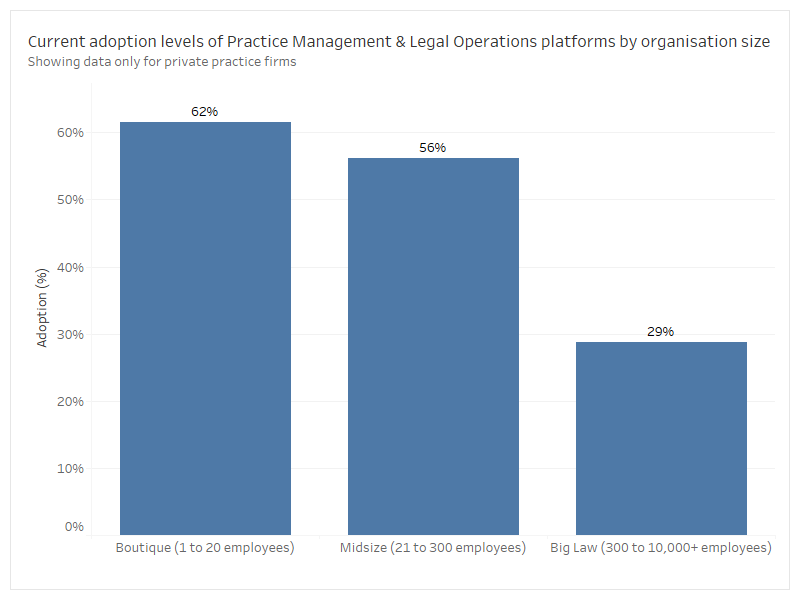

- Practice management & legal operations solutions are adopted by 50% of private practice law firms surveyed. Adoption by firm size shows boutique firms hold the largest market share, with 62% adopting practice management software.

- User experience is the strongest driver of practice management platform satisfaction, while artificial intelligence elements have relatively influential and lower satisfaction scores.

- Users are concerned about pricing and technical limitations, but demand for innovation, integration and automation remains high.

Small and midsize firms lead on practice management tech adoption

- 62% of boutique firms (1-20 employees) adopted practice management tech.

- Adoption decreases to 56% for mid size firms, and just 29% of Big Law firms.

- Smaller firms are the most likely to rely on dedicated platforms to manage admin and workflow.

Adoption of practice management & legal operations platforms is widespread, but skewed heavily toward smaller firms. 62% of boutique firms have adopted this category of legal tech, with usage declining as firm size increases. This pattern suggests that smaller firms may be more motivated to adopt streamlined, off-the-shelf systems to manage time, billing, and matter workflows.

This trend aligns with findings from the 2025 Legal Trends for Solo and Small Firms report by Clio in the UK for cloud-based practice management solutions, which reported 79-81% of solo and small firms in the UK use cloud-based practice management tools compared to just 47% of larger firms. Similarly, the 2024 Practice Management TechReport by the American Bar Association found adoption is highest among solo and small practices in the US. Larger firms are more likely to rely on custom workflows, legacy enterprise systems, and substantial in-house IT support, making adoption of all-in-one platforms slower and less central to their operations.

“Smaller firms are more agile in adopting tech that delivers quick wins. But for larger firms, adoption depends on how well platforms plug into broader systems. The value has to scale with the complexity,” Michael Johnson, Director at Agile Market Intelligence

User experience is the strongest driver for loyalty

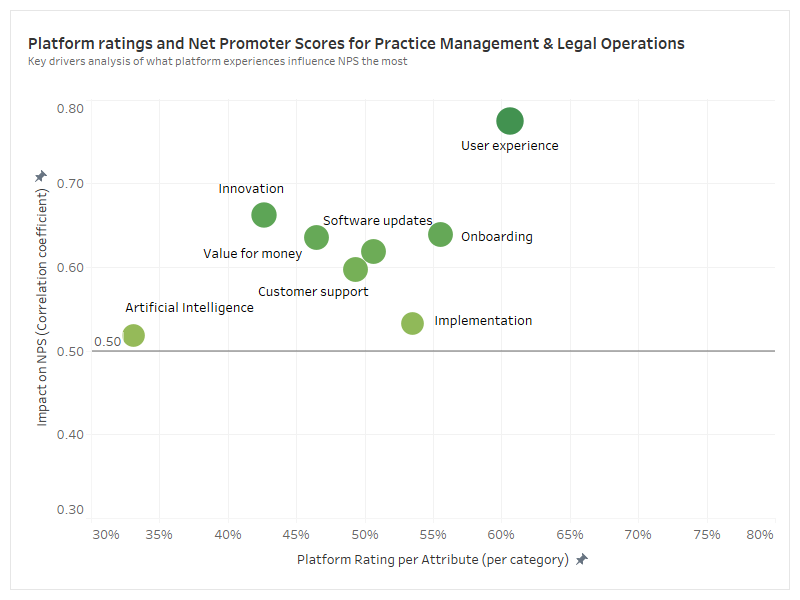

- User experience has the highest correlation with NPS for practice management platforms (r=0.78)

- Other influential attributes include innovation (r=0.66), onboarding (r=0.65) and software updates (r=0.63)

- Most platform attributes are rated between 45% and 55% positive, showing no clear standouts

We analysed responses from over 1,250 legal professionals, comparing how they rated specific aspects of their platform experience (e.g. user experience, value for money) with the Net Promoter Score (NPS) they provided, based on the question “How likely is it that you would recommend [product] to a friend or colleague?”. This analysis gives us the correlation coefficients (r), indicating the strength and direction of the relationship between each experience and their overall satisfaction. The value of r ranges from -1 to +1, with higher positive values indicating a stronger influence on NPS.

Results show that ‘user experience’ (r=0.78) is clearly the most important driver for satisfaction and loyalty for practice management & legal operations platforms; conversely elements relating to artificial intelligence have relatively less impact on NPS, and generally have lower satisfaction levels as well.

The strongest signals come from fundamentals: intuitive design, smooth onboarding and strong workflow integration. While advanced features like AI and other advanced features attract attention, lasting satisfaction is grounded on how platforms fit into day-to-day operations.

“Firms have limited tolerance for friction. If onboarding is poor or the interface feels dated, users disengage. Even widespread adoption can’t guarantee satisfaction,” - Michael Johnson

Workflow automation and time-saving features a hit, but technical gaps and pricing concerns persist

- Value for money correlates with NPS (r=0.63) but remains low-rated, comments from platform users confirm price concerns, and desire for ‘lite’ platform options.

- Legal professionals praise platform features that speed up workflows.

- Technical issues such as crashes and lag after updates are frequently mentioned.

Open-ended feedback collected in the study highlights a strong appetite for smarter, more connected systems. Users appreciate the time-saving features and workflow automation that practice management solutions offer, particularly in billing, precedents, document management, including the fast turnaround times for high volume settlements.

“Organisation is very satisfied with ***. The platform is intuitive, well-integrated, and supports our workflow efficiently”

“It’s really good it just has so many tech errors and integration problems with Microsoft.”

However, pricing sensitivity and inconsistent technical delivery are dragging down satisfaction. Many small and mid size firms, who hold most of the market share, are calling for scalability. Legal professionals are concerned about increasing fees, and express wanting ‘lite’ versions of the platforms for smaller businesses. Technical issues were also voiced out across the market, mentioning crashes and slowing down due to updates.

“*** saves me a lot of time… but the fee increases are concerning”

“'... good all-round product, but updates tend to crash the computers which is annoying”

"The bar is rising. Legal teams are no longer just looking for digital versions of manual tasks. They want platforms that fit their ecosystem and evolve with their needs," - Michael Johnson

About the research

The 2025 Agile Market Intelligence Legal Tech Review is based on survey responses collected from 1,250 legal professionals across Australia. The research was conducted between 4 February and 5 May 2025. The sample includes 914 professionals working in private practice and 269 in in-house roles, spanning a broad mix of firm sizes, locations and practice areas.